Learn more about FICO® Scores

Southland Members may access their FICO® Score for free by logging in to Digital Banking on desktop or mobile. Understanding your FICO® Scores and what they mean to you is a critical part of your financial health.

What is a FICO® Score?

FICO® Scores are the most widely used credit scores. Each FICO® Score is a three-digit number calculated from the data on your credit reports at the three major consumer reporting agencies—Experian, TransUnion and Equifax. Your FICO® Scores predict how likely you are to pay back a credit obligation as agreed. Lenders use FICO® Scores to help them quickly, consistently and objectively evaluate potential borrowers’ credit risk. Southland provides FICO® Score 9 based on Experian data, which may reviewed any time in Digital Banking. Southland updates FICO® Scores quarterly.

What goes into FICO® Scores?

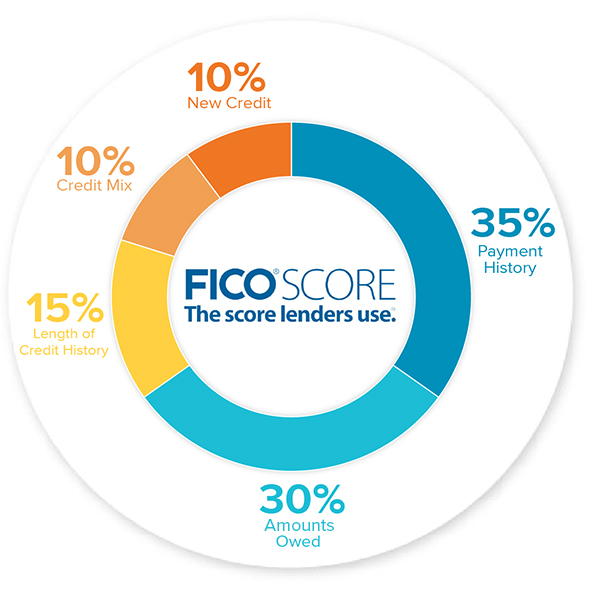

FICO® Scores are calculated from the credit data in your credit report. This data is grouped into five categories; the chart below shows the relative importance of each category.

- 35% Payment history: Whether you've paid past credit accounts on time.

- 30% Amounts owed: The amount of credit and loans you are using.

- 15% Length of credit history: How long you've had credit.

- 10% New credit: Frequency of credit inquiries and new account openings.

- 10% Credit mix: The mix of your credit, retail accounts, installment loans, finance company accounts and mortgage loans.

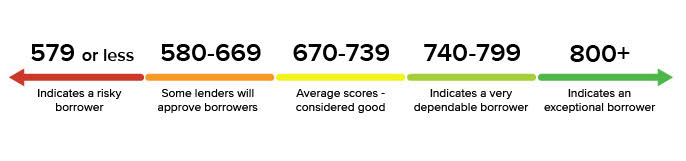

The chart below provides a breakdown of ranges for FICO® Scores found across the U.S. consumer population. Higher FICO® Scores are a result of healthy credit behaviors, and the best way to get and maintain a higher FICO® Score is to demonstrate good financial decisions over time.

How can I manage my credit and FICO® Score responsibly?

- Pay your bills on time. Delinquent payments and collections can have a major negative impact on your FICO® Scores. If you’re behind on payments, get current and stay current.

- Avoid collections. Paying off a collection account will not remove it from your credit report. It will stay on your report for seven years.

- Keep balances low. It’s okay to use your credit cards, just be careful about using a large percentage of your available credit — high utilization rates can have a major impact on your FICO® Scores.

- Do your rate shopping within a short period of time. FICO® Scores distinguish between a search for a single loan and a search for a mortgage, student or auto loan, in part by the length of time over which inquiries occur.

- Have credit and manage it responsibly. Ultimately, having a mixture of credit is a good thing — as long as you make your payments regularly and on time. Someone with no credit cards tends to be higher risk than someone who has managed credit cards responsibly.

Why is my FICO® Score different than other scores I’ve seen?

There are many different credit scores available to consumers and lenders. FICO® Scores are the credit scores used by most lenders, and different lenders may use different versions of FICO® Scores. In addition, FICO® Scores are based on credit file data from a consumer reporting agency, so differences in your credit files may create differences in your FICO® Scores.

Why do FICO® Scores fluctuate/change?

There are many reasons why a score may change. FICO® Scores are calculated each time they are requested, taking into consideration the information that is in your credit file from a consumer reporting agency at that time. So, as the information in your credit file at that CRA changes, FICO® Scores can also change. Review your key score factors, which explain what factors from your credit report most affected a score. Comparing key score factors from the two different time periods can help identify causes for a change in a FICO® Score. Keep in mind that certain events such as late payments or bankruptcy can lower FICO® Scores quickly.

Will receiving my FICO® Score impact my credit?

No. The FICO® Score we provide to you will not impact your credit.

How do I check my credit report for free?

You may get a free copy of your credit report from each of the three major consumer reporting agencies annually. To request a copy of your credit report, please visit: www.annualcreditreport.com. Please note that your free credit report will not include your FICO® Score. Because your FICO® Score is based on the information in your credit report, it is important to make sure that the credit report information is accurate.

Why is my FICO® Score not available?

There are a few possible reasons that your FICO® Score may not be available at this time. These reasons can include:

- You are a new Member of Southland Credit Union. FICO® Scores are updated on a quarterly basis in Digital Banking.

- You have not yet opted in to this free benefit

- You do not have enough credit (loan) history to have a score

- Your score was temporarily unavailable at the time of our update

- You opted out of this benefit

More education

To learn more about FICO® Scores, please review FICO® Score FAQs and Understanding FICO® Scores.